[Anchor]

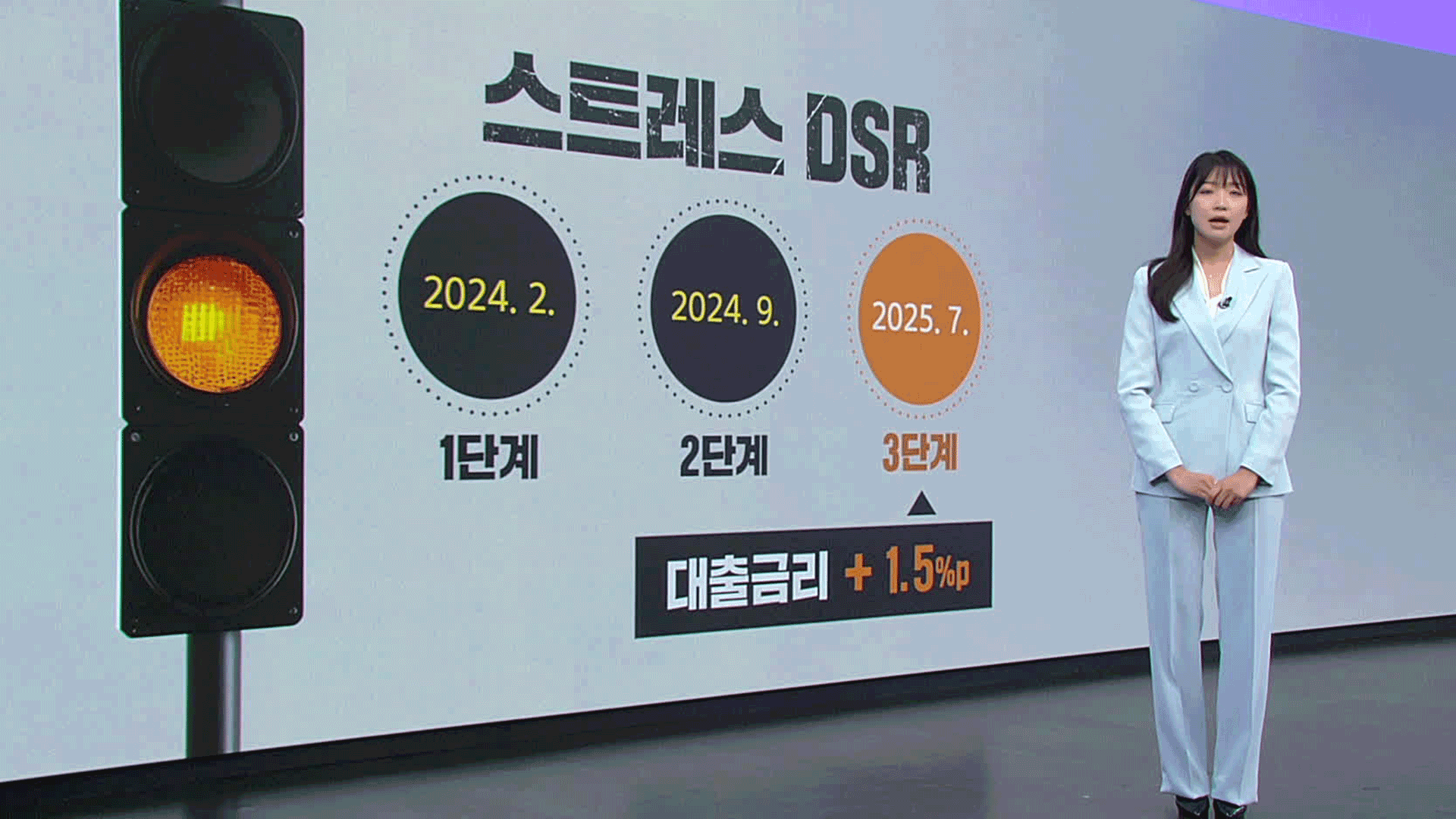

In addition to these high-intensity regulations, the three-stage stress DSR, which tightens loans further, has been implemented today (July 1).

The deposit insurance limit is expected to increase to 100 million won soon.

Reporter Choi In-young has summarized the changes in systems and policies starting in the second half of the year.

[Report]

When the signal is about to turn red, slowing down in advance is safe driving.

The 'stress DSR' has brought this habit into loans.

Although interest rates are currently rising, we do not know when the next increase will occur.

Therefore, the idea is to calculate the loan limit based on a higher interest rate.

The first stage was implemented in February last year, the second stage in September, and the final third stage is being implemented today.

An additional 1.5% will be added to the loan interest rate.

For example, if the actual interest rate is 4.0%, the calculation will be based on 5.5%.

Naturally, this results in a lower loan amount.

Assuming a 30-year mortgage with an annual income of 50 million won at an interest rate of 4.2%, the possible loan amount decreases from 300 million to 290 million, a reduction of 10 million won.

If you plan to take out a mortgage in the second half of the year, it is advisable to reassess your loan limit.

However, the severely depressed local real estate market will have a six-month grace period.

Until the end of the year, the loan limit will be calculated with an additional 0.75% as in the second stage.

What if the bank where you deposited a large sum of money goes bankrupt?

Deposit insurance has been prepared for this, and the limit will increase starting September 1.

Currently, it is 50 million won, but it will be protected up to 100 million won in the future.

This applies not only to banks but also to Saemaul Geumgo, or Community Credit Cooperatives, and various cooperatives.

The limit is calculated separately for each financial institution.

For example, if you deposit 200 million won, with 100 million in Bank A and 100 million in Bank B, you can receive 100% protection.

Swimming pools and gyms.

For those using sports facilities, a new income deduction benefit has been established.

If your total salary is below 70 million won, 30% of the payment amount for usage fees will be deducted from taxable income during year-end tax settlement.

However, membership fees and lesson fees are excluded.

About 160 livelihood policies will change starting in the second half of the year.

You can check these changes on the 'This is how it changes' website.

This is KBS News, Choi In-young.

In addition to these high-intensity regulations, the three-stage stress DSR, which tightens loans further, has been implemented today (July 1).

The deposit insurance limit is expected to increase to 100 million won soon.

Reporter Choi In-young has summarized the changes in systems and policies starting in the second half of the year.

[Report]

When the signal is about to turn red, slowing down in advance is safe driving.

The 'stress DSR' has brought this habit into loans.

Although interest rates are currently rising, we do not know when the next increase will occur.

Therefore, the idea is to calculate the loan limit based on a higher interest rate.

The first stage was implemented in February last year, the second stage in September, and the final third stage is being implemented today.

An additional 1.5% will be added to the loan interest rate.

For example, if the actual interest rate is 4.0%, the calculation will be based on 5.5%.

Naturally, this results in a lower loan amount.

Assuming a 30-year mortgage with an annual income of 50 million won at an interest rate of 4.2%, the possible loan amount decreases from 300 million to 290 million, a reduction of 10 million won.

If you plan to take out a mortgage in the second half of the year, it is advisable to reassess your loan limit.

However, the severely depressed local real estate market will have a six-month grace period.

Until the end of the year, the loan limit will be calculated with an additional 0.75% as in the second stage.

What if the bank where you deposited a large sum of money goes bankrupt?

Deposit insurance has been prepared for this, and the limit will increase starting September 1.

Currently, it is 50 million won, but it will be protected up to 100 million won in the future.

This applies not only to banks but also to Saemaul Geumgo, or Community Credit Cooperatives, and various cooperatives.

The limit is calculated separately for each financial institution.

For example, if you deposit 200 million won, with 100 million in Bank A and 100 million in Bank B, you can receive 100% protection.

Swimming pools and gyms.

For those using sports facilities, a new income deduction benefit has been established.

If your total salary is below 70 million won, 30% of the payment amount for usage fees will be deducted from taxable income during year-end tax settlement.

However, membership fees and lesson fees are excluded.

About 160 livelihood policies will change starting in the second half of the year.

You can check these changes on the 'This is how it changes' website.

This is KBS News, Choi In-young.

■ 제보하기

▷ 카카오톡 : 'KBS제보' 검색, 채널 추가

▷ 전화 : 02-781-1234, 4444

▷ 이메일 : kbs1234@kbs.co.kr

▷ 유튜브, 네이버, 카카오에서도 KBS뉴스를 구독해주세요!

- Policy changes for daily life

-

- 입력 2025-07-02 04:32:17

[Anchor]

In addition to these high-intensity regulations, the three-stage stress DSR, which tightens loans further, has been implemented today (July 1).

The deposit insurance limit is expected to increase to 100 million won soon.

Reporter Choi In-young has summarized the changes in systems and policies starting in the second half of the year.

[Report]

When the signal is about to turn red, slowing down in advance is safe driving.

The 'stress DSR' has brought this habit into loans.

Although interest rates are currently rising, we do not know when the next increase will occur.

Therefore, the idea is to calculate the loan limit based on a higher interest rate.

The first stage was implemented in February last year, the second stage in September, and the final third stage is being implemented today.

An additional 1.5% will be added to the loan interest rate.

For example, if the actual interest rate is 4.0%, the calculation will be based on 5.5%.

Naturally, this results in a lower loan amount.

Assuming a 30-year mortgage with an annual income of 50 million won at an interest rate of 4.2%, the possible loan amount decreases from 300 million to 290 million, a reduction of 10 million won.

If you plan to take out a mortgage in the second half of the year, it is advisable to reassess your loan limit.

However, the severely depressed local real estate market will have a six-month grace period.

Until the end of the year, the loan limit will be calculated with an additional 0.75% as in the second stage.

What if the bank where you deposited a large sum of money goes bankrupt?

Deposit insurance has been prepared for this, and the limit will increase starting September 1.

Currently, it is 50 million won, but it will be protected up to 100 million won in the future.

This applies not only to banks but also to Saemaul Geumgo, or Community Credit Cooperatives, and various cooperatives.

The limit is calculated separately for each financial institution.

For example, if you deposit 200 million won, with 100 million in Bank A and 100 million in Bank B, you can receive 100% protection.

Swimming pools and gyms.

For those using sports facilities, a new income deduction benefit has been established.

If your total salary is below 70 million won, 30% of the payment amount for usage fees will be deducted from taxable income during year-end tax settlement.

However, membership fees and lesson fees are excluded.

About 160 livelihood policies will change starting in the second half of the year.

You can check these changes on the 'This is how it changes' website.

This is KBS News, Choi In-young.

In addition to these high-intensity regulations, the three-stage stress DSR, which tightens loans further, has been implemented today (July 1).

The deposit insurance limit is expected to increase to 100 million won soon.

Reporter Choi In-young has summarized the changes in systems and policies starting in the second half of the year.

[Report]

When the signal is about to turn red, slowing down in advance is safe driving.

The 'stress DSR' has brought this habit into loans.

Although interest rates are currently rising, we do not know when the next increase will occur.

Therefore, the idea is to calculate the loan limit based on a higher interest rate.

The first stage was implemented in February last year, the second stage in September, and the final third stage is being implemented today.

An additional 1.5% will be added to the loan interest rate.

For example, if the actual interest rate is 4.0%, the calculation will be based on 5.5%.

Naturally, this results in a lower loan amount.

Assuming a 30-year mortgage with an annual income of 50 million won at an interest rate of 4.2%, the possible loan amount decreases from 300 million to 290 million, a reduction of 10 million won.

If you plan to take out a mortgage in the second half of the year, it is advisable to reassess your loan limit.

However, the severely depressed local real estate market will have a six-month grace period.

Until the end of the year, the loan limit will be calculated with an additional 0.75% as in the second stage.

What if the bank where you deposited a large sum of money goes bankrupt?

Deposit insurance has been prepared for this, and the limit will increase starting September 1.

Currently, it is 50 million won, but it will be protected up to 100 million won in the future.

This applies not only to banks but also to Saemaul Geumgo, or Community Credit Cooperatives, and various cooperatives.

The limit is calculated separately for each financial institution.

For example, if you deposit 200 million won, with 100 million in Bank A and 100 million in Bank B, you can receive 100% protection.

Swimming pools and gyms.

For those using sports facilities, a new income deduction benefit has been established.

If your total salary is below 70 million won, 30% of the payment amount for usage fees will be deducted from taxable income during year-end tax settlement.

However, membership fees and lesson fees are excluded.

About 160 livelihood policies will change starting in the second half of the year.

You can check these changes on the 'This is how it changes' website.

This is KBS News, Choi In-young.

-

-

최인영 기자 inyoung@kbs.co.kr

최인영 기자의 기사 모음

-

이 기사가 좋으셨다면

-

좋아요

0

-

응원해요

0

-

후속 원해요

0

오늘의 핫 클릭

실시간 뜨거운 관심을 받고 있는 뉴스

헤드라인

이 기사에 대한 의견을 남겨주세요.